The Engines of Growth in Emerging Markets and Asia

Small companies present compelling alpha opportunities.

Subscribe NowOverview

- The Emerging Market and Asia universe of small companies is vast, deep and diverse. It offers numerous ways to play distinct themes, yet research coverage of opportunities is patchy.

- A disciplined investment process, along with active in-depth research and investment experience is key to finding resilient and successful small companies.

- We share two case studies to illustrate our investment approach.

For investors, small companies personify the notion that less is more, or more specifically, that less offers the prospect of more. Businesses setting out on a path of innovation, ingenuity or shrewd expansion, offer the tantalizing possibility that in the future they will become established, cash-rich, profitable players with formidable competitive advantage – even household names and corporate stars.

In emerging markets, the road to expansion for small businesses can be fast. A widget-maker’s product can align with exploding domestic consumer demand or become snapped up by corporate giants in developed markets. Take, for example, Sunny Optical, a Hong Kong-listed manufacturer of optical-products for phones and cameras. Today it’s valued at US$13 billion, a decade ago its market cap was US$1 billion. Similarly, a mall operator in India has seen its market cap quadruple since 2013.

Breadth of opportunity

In Asia and the emerging markets, the universe of small companies – often defined as publicly-listed businesses with market values of between US$100 million and US$5 billion – is vast, deep and diverse (see Figure A).

In Saudi Arabia, for example, it’s a challenge to get large-cap exposure to consumer discretionary stocks whereas with small caps it isn’t a problem.

Small caps can be found in a multitude of sectors and industries, offering investors the potential to get exposure to nascent and fast-growing themes. In the MSCI Emerging Markets Index for example around 40% of value resides in five sub-sectors. In comparison, 40% MSCI Emerging Markets Small Cap Index sits across 17 sub-sectors, including biotechnology, real estate development and industrial machinery. It’s a similar picture in Asia (see Figure B).

Small-cap companies are often in markets that are at differing stages of the economic cycle and in contrasting phases of recovery from COVID 19. Small business, by nature, can also be left alone by political tensions and regulatory interventions. In China, for example, the recent regulatory clampdown on large-cap behemoths signaled the government’s desire to create a better balance of wealth across society and across company sizes. That has provided a relative tailwind for small caps in that country.

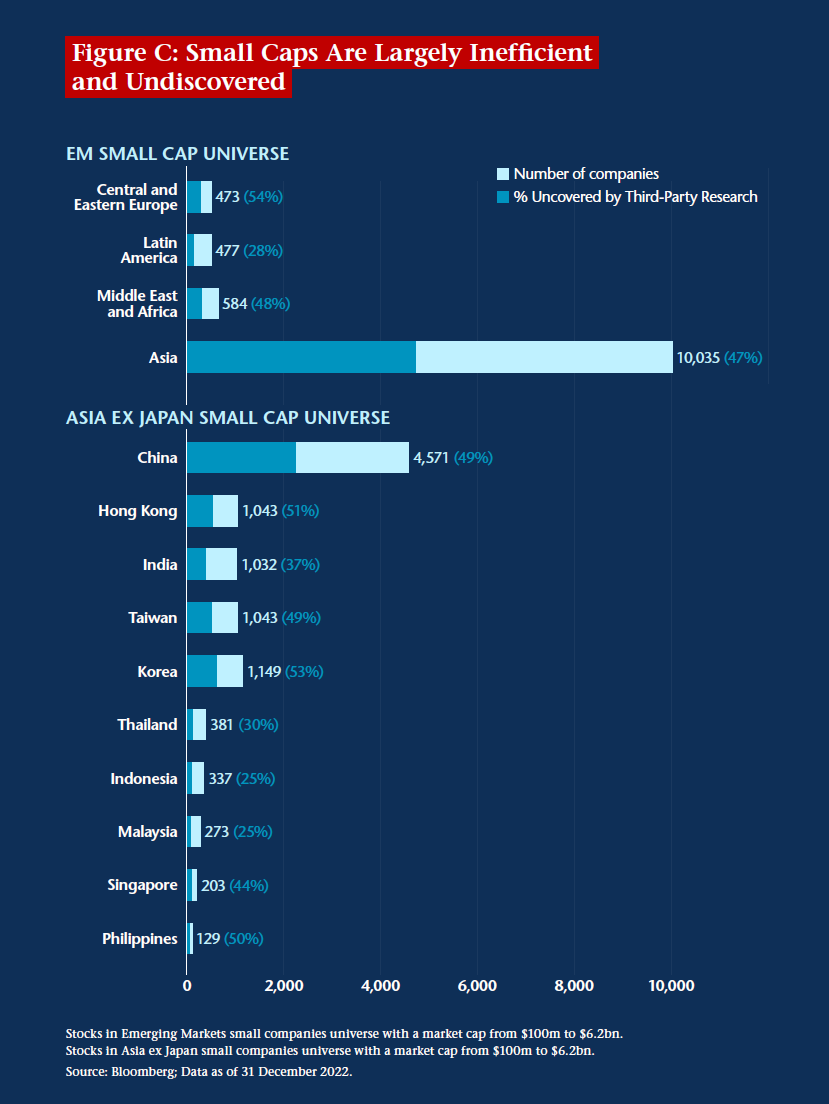

One of the most enticing attributes of small companies is their patchy research coverage. Almost half of emerging market small-cap stocks and Asia small-cap stocks aren’t covered by third-party analysts (see Figure C). Some investors may interpret a lack of analyst coverage as an indication of higher risk but for the active portfolio manager this is an opportunity to find mispriced stocks and realize value.

The key to finding these alpha opportunities is in-depth, on-the-ground fundamental research and careful portfolio construction. And we would argue that it is simpler for active managers to analyze smaller companies as they tend to be single-vertical, single-country businesses as opposed to large caps which can often be complex multi-vertical, multi-country conglomerates.

The key to finding small-cap alpha opportunities is in-depth, on-the-ground fundamental research and careful portfolio construction.

Small company challenges

Small-cap companies, with developing business models, evolving profitability and balance sheets, can inherently present higher risk for investors than bigger, established companies. That said, there are no guarantees for a business of any size. Large caps are concentrated in a handful of large sectors and in an event like the Global Financial Crisis (GFC), U.S. large-cap companies – dominated by financials and real estate – faced disproportionate turbulence.

One of the main risks to manage with small companies is liquidity. In our approach, we only increase position sizes as operational business milestones are passed and as our conviction grows. While small caps may have weaker balance sheets on average to bigger companies, the huge universe means avoiding overleveraged companies is straightforward. We steer clear of companies with high financial leverage, preferring ones with less debt and the ability to fund expansion through internal cash generation.

Shareholder liquidity also needs to be carefully managed with small-cap investing. It can vary depending on the prevalence of family shareholdings, and retail-versus-institutional ownership, and between markets. China’s domestic A-shares market, for example, is relatively liquid compared with other emerging markets.

Lessons of experience

Investment experience is critical for enhancing the probability of selecting resilient and successful small companies in the emerging markets universe. When we analyze a new prospect, we draw heavily on our past sector and company knowledge.

It is essential to take the time for in-depth company analysis – involving interviewing several layers of management as well as talking to clients, suppliers and competitors – while working on a timeframe that can take advantage of short-term volatility.

We believe that some of the most important attributes are pricing power, visibility of earnings, capital allocation, capital structure and addressable market. Companies cannot grow earnings sustainably through cost optimization. They need sales growth. The potential to deliver above average revenue growth for a long period of time requires picking companies addressing large and/or fast-growing market opportunities.

Just as visiting different companies provides relevant investment insights, so does covering such a diverse mix of countries. Macro dynamics and cycles differ country by country. This sometimes provides helpful potential playbooks; events that played out in one market may occur in a similar manner later in another country.

Emerging Markets and Asia have long provided a fertile hunting ground for active managers. Given the low research coverage and diversity of its universes, we believe smaller companies present even more compelling alpha opportunities. Nowhere else, in our view, can investors gain exposure to as many unique companies that are typically under-researched and often inefficiently priced compared to large companies. Smaller companies can also provide direct access to high-growth domestic consumption sectors that typically cater to a fast-expanding and resilient middle class. They also offer an opportunity to invest in innovation and to partner with shareholder-friendly entrepreneurs who may well become future captains of industry.

It is essential to take the time for in-depth company analysis – involving interviewing several layers of management as well as talking to clients, suppliers and competitors – while working on a timeframe that can take advantage of short term volatility.

Small caps on the groundA couple of our holdings illustrate our smaller companies investment approach: Siam Wellness Group Poya International In our view, standalone home and cosmetics stores represent significant opportunities for the company in addition to the organic expansion potential of its core segment. Looking forward, we believe the company is well-positioned to execute on its long-term growth plan. |

Investments involve risk. Investing in international, emerging and frontier markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Additionally, investing in emerging and frontier securities involves greater risks than investing in securities of developed markets, as issuers in these countries generally disclose less financial and other information publicly or restrict access to certain information from review by non-domestic authorities. Emerging and frontier markets tend to have less stringent and less uniform accounting, auditing and financial reporting standards, limited regulatory or governmental oversight, and limited investor protection or rights to take action against issuers, resulting in potential material risks to investors. Investing in small- and mid-size companies is more risky than investing in larger companies as they may be more volatile and less liquid than large companies. Pandemics and other public health emergencies can result in market volatility and disruption.

Definitions

Alpha: Alpha, a commonly quoted indicator of investment performance, is defined as the excess return on an investment relative to the return on a benchmark index.

MSCI All Country Asia ex Japan Index: The MSCI All Country Asia ex Japan Index is a free float–adjusted market capitalization–weighted index of the stock of markets of China, Hong Kong, India, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan and Thailand.

MSCI All Country Asia ex Japan Small Cap Index: The MSCI All Country Asia ex Japan Small Cap Index is a free float–adjusted market capitalization–weighted small cap index of the stock markets of China, Hong Kong, India, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan and Thailand.

MSCI Emerging Markets Index: The MSCI Emerging Markets Index Captures large and mid-cap representation across 24 Emerging Markets (EM) countries. With 1,138 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. EM countries include: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Qatar, Russia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates.

MSCI Emerging Markets Small Cap Index: The MSCI Emerging Markets Small Cap Index is a free float-adjusted market capitalization-weighted index of the stock markets of Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Qatar, Russia, Saudi Arabia, South Africa, South Korea, Taiwan, Thailand, Turkey and United Arab Emirates.