How Small Caps Can Navigate China’s Growth Challenges and India’s Valuations

Vivek Tanneeru reviews the positioning of the Matthews Asia Small Companies Fund.

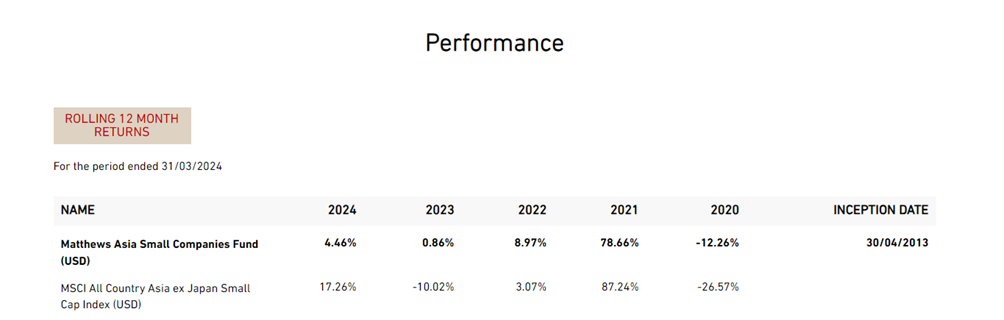

Exposure to China has been a major challenge for many Asia ex Japan and emerging markets portfolios over the past three years but good stock picking can help navigate these headwinds. The Matthews Asia Small Companies Fund, for example, has been significantly overweight to China in the last three years and yet the portfolio generated 2.1% annualised alpha versus its benchmark, the MSCI AC Asia ex Japan Small Cap Index. Strong stock picking helped the Fund overcome the near-term hurdles of being overweight to China and at the same time allowed the portfolio to remain positioned for what we think will be a strengthening recovery in the world’s second largest economy.

It is one of the reasons why the Matthews Asia Small Companies Fund’s positioning to China hasn’t changed significantly in the past 12 months despite continued weakness in Chinese equity markets. The Fund’s combined exposure to China and India usually ranges between 40%-70%. Given the Fund’s neutral weighting of about 30% to India, the combined exposure was about 62% at the end of March.

“India and China have potentially the most powerful growth engines in the world.”

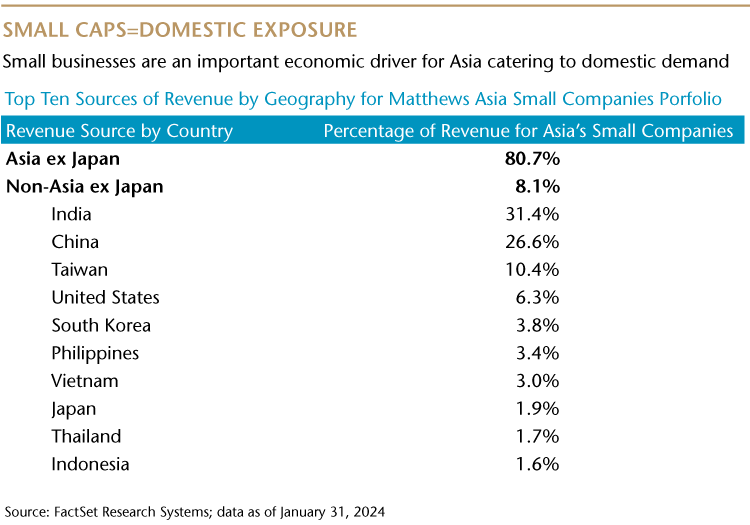

We believe China, and to a lesser extent India, are the only two markets outside the U.S. where small cap holdings have the potential to double or triple revenue in a very short space of time. In short, these markets have potentially the most powerful growth engines in the world, in our view. But active investing untethered to index benchmarks is the key to harnessing this growth. The MSCI AC Asia ex Japan Small Cap Index, for example, ranks China and Hong Kong behind India, Taiwan and South Korea in terms of benchmark weighting. The index also doesn’t include the onshore China A-shares market, which is 80% of China’s investable universe.1 In sum, we believe the index doesn’t reflect the opportunities that exist for investors in the market; hence we are comfortable with the Fund’s allocation to China. We think it remains an attractive market for small-cap companies to grow over the long-term.

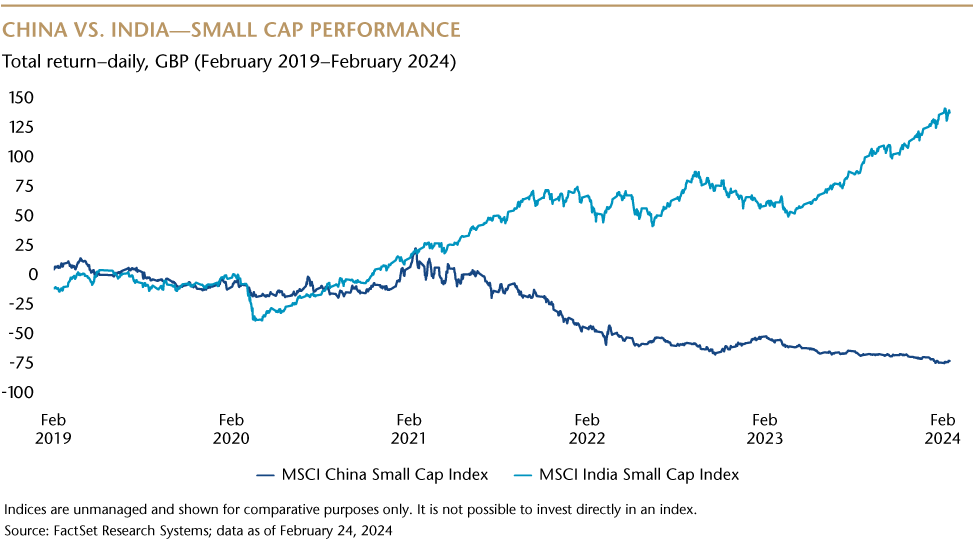

While investor sentiment to China is weak, the opposite is true for India where there has been significant investor inflows into small and mid-cap funds. The Matthews Asia Small Companies Fund was overweight to India until the end of 2022—an allocation that positively added to performance. Since then, the Fund’s exposure has reduced to a neutral weight compared to the index.

Valuing China and India

India has traditionally been an expensive market compared to peers but today it is trading at about a 33% premium to its own long-term average. Small-cap valuations are near all-time highs. Compared with China, the valuation difference is huge. Consequently, on a stock-by-stock basis, we have been taking profits on the margin over the past 18 months in India and our two largest holdings in India are what we consider to be value businesses. This all said, we are firm believers in India’s long-term potential. The economy is doing well, corporate earnings appear solid and the country is now truly industrializing.

Outside of China and India, the portfolio remains underweight in Taiwan and South Korea, with a tilt toward the developing countries in the ASEAN region such as Vietnam and Indonesia where we are finding more attractive growth opportunities versus Singapore and Malaysia. Vietnam has been one of the biggest beneficiaries of manufacturing diversifying away from China and while it is going through some headline geopolitical risks it is nothing too worrying for the portfolio, in our view.

Taiwan is at the epicentre of the artificial Intelligence (AI) revolution and while our mandate doesn’t allow us to invest in the mega-cap companies that dominate this theme, we believe there are plenty of small cap opportunities within the supply chain. Even though the Fund is underweight Taiwan, it has built considerable exposure to the AI revolution theme and this has generated solid performance in the recent years.

Style agnostic for maximum opportunity

Some supply chains, particular technology-related ones, of course, have been in the crosshairs of geopolitics and 2024 is a big election year. While we’re not expecting any surprises in terms of India’s general election, the U.S. election is something we are mindful of. Our investment approach generally avoids investing in companies that may get entangled in U.S.-China political tensions. This means, particularly in China, that we focus on domestic consumption, health care, and industrials, as well as investing in mainstream, non-controversial tech companies.

We also favour a style agnostic approach. This has been key to the fund’s outperformance over the long-term. In the last five years, for example, we have seen a wide range of market conditions with both value and growth styles outperforming at different periods. Our focus on valuations and diversifying sources of alpha across styles, markets and different company business models helped to deliver performance throughout these periods.

It is our view, that valuations are attractive in many small cap areas, particularly in China. And we believe these are opportunities with robust long-term growth potential. So while the past 12 months have been tough, we believe the Fund is well-positioned for the near term and beyond.

Vivek Tanneeru

Portfolio Manager

Matthews Asia

1Source: Data from Bloomberg as of June 30,2023

Source: Brown Brothers Harriman (Luxembourg) S.C.A.

All returns over 1 year are annualized.

Performance details provided are based on a NAV-to-NAV basis with any dividends reinvested, and are net of management fees and other expenses. Performance data has been calculated in the respective currencies stated above, including ongoing charges and excluding subscription fee and redemption fee you might have to pay.

All performance quoted represents past performance and is not indicative of future performance. Investors may not get back the full amount invested. Investors investing in funds denominated in non-local currency should be aware of the risk of currency exchange fluctuations that may cause a loss of principal.

The investment policy of the Fund was changed on 15 December 2021. The performance prior to this date was achieved under circumstances that no longer apply.

Data as of 31 January 2023, in USD, I (Acc) for the Fund.

Risk Considerations

The value of an investment in the Fund can go down as well as up and possible loss of principal is a risk of investing. Investments in international, emerging and frontier market securities may involve risks such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation, which may adversely affect the value of the Fund's assets. The Fund invests in holdings denominated in foreign currencies, and is exposed to the risk that the value of the foreign currency will increase or decrease. The Fund invests primarily in equity securities, which may result in increased volatility. The Fund invests in smaller companies, which are more volatile and less liquid than larger companies. These and other risks associated with investing in the Fund can be found in the Prospectus.

Important Information

For Institutional/Professional Investors Only

This is a marketing communication. This document is not a Prospectus/Offering Document and does not constitute an offer to the public. No public offering or advertising of investment services or securities is intended to have taken effect through the provision of these materials. Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before making an investment decision. The current prospectus, Key Investor Information Document or other offering documents ("Offering Documents") contain this and other information. Please refer to the prospectus of the UCITS and to the KIID before making any final investment decisions.

The Fund is a sub-fund of Matthews Asia Funds SICAV, an umbrella fund, with segregated liability between sub-funds, established as an open-ended investment company with variable capital and incorporated with limited liability under the laws of Luxembourg.

Investment involves risk. Past performance is no guarantee of future results. The value of an investment in the Fund can go down as well as up. This is not intended for distribution or use in any jurisdiction in which such distribution, publication, issue or use is not lawful. Investors should not invest in a Fund solely based on the information in this document. An investment in Matthews Asia Funds may be subject to risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Additionally, investing in emerging and frontier securities involves greater risks than investing in securities of developed markets, as issuers in these countries generally disclose less financial and other information publicly or restrict access to certain information from review by non-domestic authorities. Emerging and frontier markets tend to have less stringent and less uniform accounting, auditing and financial reporting standards, limited regulatory or governmental oversight, and limited investor protection or rights to take action against issuers, resulting in potential material risks to investors. Pandemics and other public health emergencies can result in market volatility and disruption. The current prospectus, Key Investor Information Document or other offering documents (“Offering Documents”) contain this and other information and can be obtained by visiting global.matthewsasia.com. It is the responsibility of any persons wishing to subscribe for shares to inform themselves of and to observe all applicable laws and regulations of any relevant jurisdictions. Prospective investors should inform themselves as to the legal requirements and tax consequences within the countries of their citizenship, residence, domicile and place of business with respect to the acquisition, holding or disposal of shares, and any foreign exchange restrictions that may be relevant thereto.

An investment in the Matthews Asia Funds is not available in all jurisdictions. The Fund’s shares may not be sold to citizens or residents of the United States or in any other state, country or jurisdiction where it would be unlawful to offer, solicit an offer for, or sell the shares. No securities commission or regulatory authority has in any way passed upon the merits of an investment in the Fund or the accuracy or adequacy of this information or the material contained herein or otherwise.

Matthews Asia is the brand for Matthews International Capital Management, LLC and its direct and indirect subsidiaries.

The MSCI China Small Cap Index is a free float-adjusted market capitalization-weighted small cap index of the Chinese equity securities markets, including H shares listed on the Hong Kong exchange, B shares listed on the Shanghai and Shenzhen exchanges, Hong Kong-listed securities known as Red Chips (issued by entities owned by national or local governments in China) and P Chips (issued by companies controlled by individuals in China and deriving substantial revenues in China), and foreign listings (e.g., ADRs).

The MSCI India Small Cap Index is designed to measure the performance of the small cap segment of the Indian market. With 253 constituents, the index represents approximately 14% of the free float-adjusted market capitalization of the India equity universe.

The MSCI All Country Asia ex Japan Small Cap Index is a free float–adjusted market capitalization–weighted small cap index of the stock markets of China, Hong Kong, India, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan and Thailand.

Indices are for comparative purposes only and it is not possible to invest directly in an index.

In the UK, this document is only made available to professional clients and eligible counterparties as defined by the Financial Conduct Authority (“FCA”). Under no circumstances should this document be forwarded to anyone in the UK who is not a professional client or eligible counterparty as defined by the FCA. Issued in the UK by Matthews Global Investors (UK) Limited (“Matthews Asia (UK)”), which is authorised and regulated by the FCA, FRN 667893.