Stepping Back From the Brink?

A trade deal is expected when Presidents Trump and Xi meet, but even if the talks fail, Sinology explains why China can mitigate the impact and maintain the world's best consumer story.

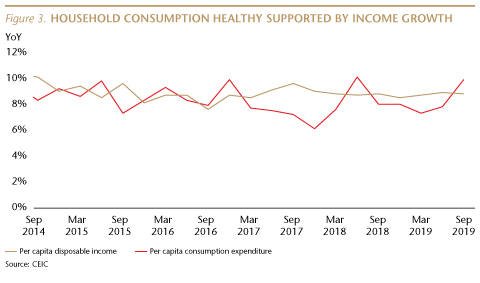

"Household consumption, China's key economic driver, remains healthy, up 9.9% YoY in 3Q19 vs. 8% a year ago."

With Donald Trump saying he expects to sign a “fantastic” deal with Xi Jinping next month in Santiago, Chile, the U.S. may be stepping back from the brink of escalating a tariff dispute into a full-blown trade war with the world's second largest economy. It is likely that some form of a deal will be reached, but even if the negotiations fail, just published third-quarter macro data suggests that China has the capacity to mitigate the impact of a broader dispute and maintain the world's best consumer story.

What to expect in Santiago

Progress earlier this month in the U.S. – China trade talks represented an important reset in the tone of bilateral relations. There is no guarantee that both sides can agree on the details before Trump and Xi meet during the November 16-17 APEC (Asia-Pacific Economic Cooperation) summit in Chile, but the shift in Trump's attitude is very significant in an administration where the president's feelings are more important than the substantive issues in front of negotiators.

Trump's enthusiastic comments leave me optimistic that a formal deal can be concluded next month. Stating that the two sides had already “come to a deal on intellectual property, financial services,” as well as “a tremendous deal for the farmers,” Trump said, “I have very little doubt that we'll be able to get this thing finalized now. It's not overly complex.”

The president remarked “there was a lot of friction between the United States and China. And now, it's a lovefest.” He also provided some domestic political cover for Xi, describing the deal as “fantastic for China” as well as “fantastic for the United States.”

I remain convinced that both sides are highly motivated to conclude a deal. Trump appears to recognize that a deal is better than no deal for his re-election prospects. No deal would mean continued taxes on Chinese goods, paid for by American families and businesses. No deal would mean a continued Chinese boycott of American soybeans, which is contributing to harsh conditions for farmers in politically important states. No deal would mean continued economic uncertainty, which is leading to weaker corporate CapEx and worries about a recession.

The tariffs are not a huge problem for Xi, as China is no longer an export-led economy, but failure to conclude a deal would open up the risk that a trade war leads to restrictions on China's access to American tech, everything from semiconductors to research collaboration. That would be a significant setback to China's economic growth, which Xi wants to avoid.

Details of the tentative deal have not been disclosed, so we don't know whether the disruption caused by the tariff dispute will have been worthwhile (I doubt it), but in my view that is of secondary importance. Even if the deal only takes the trading relationship back to where it was a couple of years ago, that is important—lessening business uncertainty and creating an opportunity for reducing bilateral tensions across a wide range of issues, from technology to investment.

But, what if I'm wrong and there is no deal in Santiago?

If a deal isn't reached, I will be very concerned about the longer-term relationship between the U.S. and China—the country which accounts for one-third of global economic growth, larger than the combined share of growth from the U.S., Europe and Japan. Failure to reach any deal would have a profound impact on the global economy. But, I will be less worried about the near-term impact on China, as the main engine of its growth— domestic demand—remains healthy, and Beijing has a significant store of dry powder it could deploy to mitigate the impact of an all-out trade war with Washington.

Still the world's best consumer story

Last year, net exports (the value of a country's exports minus its imports) were equal to less than 1% of China's GDP. And the contribution from the secondary part of GDP, manufacturing and construction, has been declining. This will be the eighth consecutive year in which the tertiary part of GDP, consumption and services, is the largest part; last year, three-quarters of China's economic growth came from consumption.

This is especially important right now, because the domestic demand story should continue to be fairly well insulated from the impact of the Trump tariff dispute.

Decelerating, but still fast

Most aspects of the Chinese economy have been decelerating gradually over the past decade, including the inflation-adjusted (real) growth rate of retail sales. This is due in part to the rapid expansion of the base: the dollar value of retail sales in China was equal to 91% of U.S. retail sales last year, up from 36% a decade earlier. But real retail sales rose 6.4% YoY during the first nine months of this year, compared to 1.6% in the U.S.

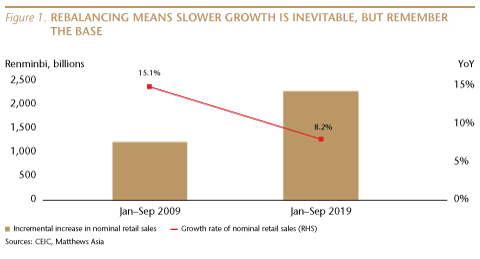

The base effect is also important in gauging the impact of slower growth. Nominal retail sales, for example, rose 8.2% in the first three quarters of this year, far slower than the 15.1% pace a decade ago. But, because the base is now 252% larger, the incremental expansion in nominal retail sales so far this year was over 90% larger than the same period in 2009. (And it is worth noting that over that time, the retail price index for consumer goods rose only 19%.)

Over the last five years, the real growth rate of retail sales in China slowed by an average of 0.9 percentage points each year, and during the first three quarters of this year, the growth rate also slowed by 0.9 percentage points, compared to the same period in 2018.

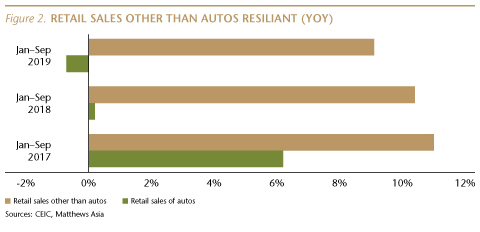

This year and in 2018, sharply weaker auto sales—due to structural issues, including the removal of subsidies that brought forward demand in earlier years—contributed significantly to slower growth in overall retail sales. Excluding autos, nominal retail sales rose 9.1% during the first nine months of this year, compared to 10.4% during the same period last year and 11% in 2017.

Nike is one example of the resilience of China's consumers. The company's most recent quarter marked the 21st consecutive quarter of double-digit revenue growth in Greater China, and revenue was up 27% YoY, compared to 4% in North America.

Here is another perspective: household consumption—a metric which includes services as well as goods—rose 9.9% YoY in 3Q19, up from 7.3% in 1Q19 and 8% a year ago. This acceleration reflects the rising share of consumer spending on services, as well as the strength of spending on services, including education and travel.(Spending on education, culture and recreation is up 14% this year, for example.) Services now account for 51% of household consumption, up from 40% in 2008.

Phenomenal income growth

This consumer story has been fueled by phenomenal income growth. Real income rose 5.8% YoY during 3Q19, a bit slower than 6.3% a year ago. Over the last decade, real income rose 120% in China, compared to a 17% increase in the U.S.

A key driver of income growth has been the rise of entrepreneurs. There were no privately owned firms in China when I first worked there in 1984, but now 87% of urban employment is by small, private companies.

And I think the consumer story is sustainable, in part because Chinese households still save about 27% of their disposable income, compared to an 8% savings rate in the U.S.

Manufacturing has been weaker, but is less important

Manufacturing has been weak this year, although there was a modest rebound last month. For the first three quarters, industrial value-added rose 5.6% YoY, down from 6.4% a year ago. Manufacturing investment was even weaker, up only 2.5% year-to-date, compared to 8.7% a year ago.

Modest impact has led to a modest stimulus

In my view, the impact of the tariff dispute on the Chinese economy has been modest. A bigger contributor to slower growth has been the Chinese government's ongoing campaign to reduce risks in the financial system, which has led to a sharp crackdown in off-balance sheet, or shadow credit, which declined 7.9% YoY in September. This has reduced systemic risks, but it has also meant that the firms that relied on non-standard credit sources, especially small private companies, have struggled (even more than usual) to get access to credit.

It is a positive sign that Beijing has not responded to slower growth by allowing a resurgence of shadow credit.

Key stimulus levers not yet pulled

The growth rates of credit and infrastructure investment—always the first two stimulus levers the government pulls when it is worried about unemployment—also signal that Beijing feels the economy is reasonably healthy.

Aggregate credit outstanding rose 10.9% YoY last month, the same pace as in August and slightly lower than 11.2% a year ago. Credit isn't tight—it is rising faster than nominal GDP growth—but there is no sign of significant stimulus. This leaves room for stimulus should growth slow more sharply if the trade dispute worsens.

Beijing also has room to cut rates if needed. During 1H19, the weighted average lending rate was 5.7%.

There is additional dry powder on the fiscal side, as the government has so far refrained from turning on its traditional public infrastructure stimulus taps. Infrastructure investment rose only 4.5% during the first three quarters, up slightly from 3.3% a year ago, but much lower than the 19.8% pace two years ago.

Overall, within the context of the steady, gradual deceleration which has been underway for a decade, the most important driver of China's economy, consumption, is holding up well.

Regards,

Andy Rothman

Investment Strategist

Matthews Asia

Sources: Matthews Asia, CEIC