China’s Consumers Get Their Mojo Back

China’s economy has turned the corner, and is on a path towards a gradual, domestic demand-driven recovery. Andy Rothman outlines the reasons why China’s recovery is likely to be sustainable.

Key Takeaways

- 1Q23 data strengthens my conviction that China’s economy is in the early stages of a gradual, consumer-led recovery that is likely to be sustained by accommodative government policy and large household savings.

- Strong new home sales, as well as a sharp jump in spending at bars and restaurants, signals that consumers have begun to recover from last year’s COVID-related trauma and are ready to return to normal life.

- There is a risk of another government economic policy mistake, but that is a low probability, given Xi Jinping’s priority of supporting a consumer-led recovery.

- U.S.-China relations will remain strained, but both sides understand that a further deterioration would be bad for both economies, meaning a crisis is unlikely.

- An active approach towards investing in China, focused on companies selling goods and services to Chinese consumers, can help mitigate the impact of political tensions.

I wrote in March that China opportunities outweigh risks for investors. New data for the first quarter strengthens my conviction that China’s economy is in the early stages of a gradual, consumer-led recovery that is likely to be sustained by accommodative government policy and large household savings. China is on track to drive more global economic growth than the U.S., Europe and Japan combined.

There are, of course, risks to this recovery story. The first is that the Chinese government might adopt policies which stymie growth. That was a problem in recent years, but I think this is a very low probability risk now, because Xi Jinping’s priority is to support a consumer-led economic recovery. The return to China of its most prominent entrepreneur, Alibaba founder Jack Ma, after a year outside the country, signals Xi’s understanding that he needs to create a better regulatory environment for the private companies that drive China’s economy.

The second key risk to the sustainability of the economic recovery now underway is a potential crisis in U.S. – China relations. While I expect the political relationship to remain strained, I think a crisis is only a medium-level risk, because Xi and Joe Biden are pragmatic, and recognize that a further deterioration in relations would be detrimental to each of their economies, as well as to their political prospects. In an April 20 speech, Treasury Secretary Janet Yellen suggested that the Biden administration is now taking a more constructive approach to Beijing. “We seek a healthy economic relationship with China: one that fosters growth and innovation in both countries.”

Additionally, an active approach towards investing in China, focused on companies selling goods and services to Chinese consumers, can help mitigate the impact of political strains.

Consumer confidence is back

China’s economy has clearly turned the corner, and is on a path towards a gradual, domestic demand-driven recovery. Confidence among Chinese households and entrepreneurs began to return in the first two months of the year and strengthened further in March. Retail sales, home sales, manufacturing and investment all improved in the first quarter compared to the fourth quarter of last year. Sales at restaurants and bars picked up strongly, suggesting that many Chinese have begun to shake off last year’s COVID-related trauma, and are ready to socialize and spend again.

China’s GDP expanded 4.5% year-over-year (YoY) in the first quarter of the year, the fastest pace in four quarters. The 2.2% quarter-on-quarter (QoQ) expansion is the fastest since the first quarter of 2021. More importantly, domestic demand led the way, with consumption accounting for 67% of GDP growth, the largest consumption share over the last four quarters.

In January, I wrote that I didn’t expect this turnaround to begin until the second quarter, but it is clear that the gradual recovery is already well underway. It began earlier than I expected for two, COVID-related reasons. First, there was not a second wave of cases after the massive domestic travel associated with the Lunar New Year holiday in late January. Second, local governments have not reverted to the use of lockdowns, eliminating that worry for consumers and companies.

The recovery is likely to be sustainable, in large part due to the resilience of Chinese families and entrepreneurs. And it will be supported by more pragmatic government regulatory policies, as well as a partial drawdown of the massive accumulation of household bank deposits since the start of the pandemic.

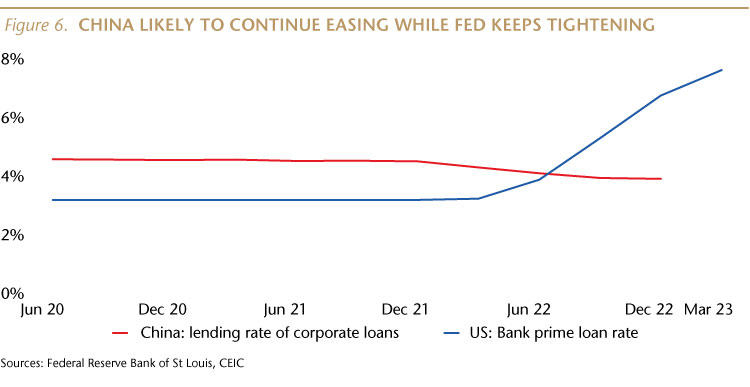

With Beijing likely to remain the only major government engaged in easing of fiscal and monetary policy—while much of the world is tightening—China may once again be the engine of global economic growth. (The consumer price index rose by only 1.3% YoY through the first quarter, and should remain relatively low for the full year, so inflation will not jeopardize monetary policy easing.)

Following are some highlights from the macro data for the first quarter of 2023.

Consumer spending

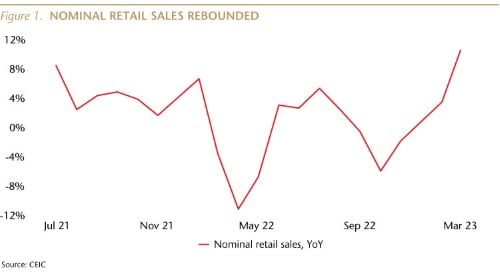

Consumer spending on goods and services, the largest part of the economy, improved significantly in the first quarter, including a March acceleration. Nominal retail sales rose 10.6% YoY in March, the strongest month since July 2021. First quarter nominal retail sales were up 5.8% YoY, a significant improvement over the last quarter of 2022. While it hasn’t yet caught up to the 8.3% pace during the first quarter of pre-COVID 2019, consumer spending is clearly heading in the right direction.

CONSUMERS BEGAN TO SHAKE OFF COVID TRAUMA IN 1Q23

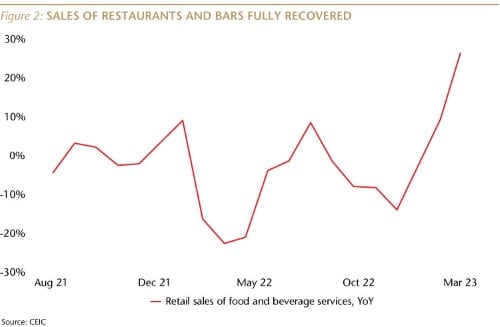

The most impressive data point is sales at restaurants and bars, which improved strongly, suggesting that many Chinese have begun to recover from last year’s COVID-related trauma and are ready to return to normal life. Restaurant and bar sales rose 26.3% YoY in March, following a 9.2% rise in January/February, up sharply from declines of -14% in December and -8% in November. Sales at restaurants and bars last month were 9% higher than in pre-COVID March 2019.

This spending was fueled by a 3.8% YoY rise in real (inflation-adjusted) income, the fastest pace since the second quarter of 2022.

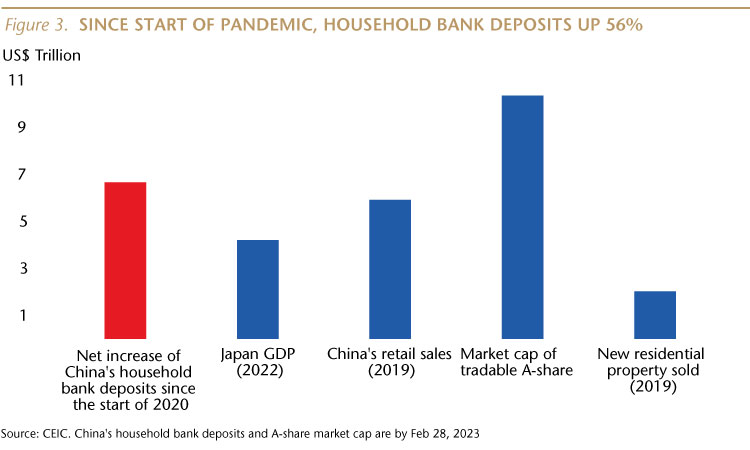

Consumer spending and confidence is also supported by the 56% rise in family bank balances from the start of 2020, as Chinese households were in savings mode during zero-COVID. The net increase in household bank accounts is equal to US$6.7 trillion, which is greater than the GDP of Japan in 2022, and equal to 113% of China’s 2019 retail sales. This is significant fuel for a continuing consumer spending rebound, as well as a recovery in mainland equities, where domestic investors hold about 95% of the market.

Property

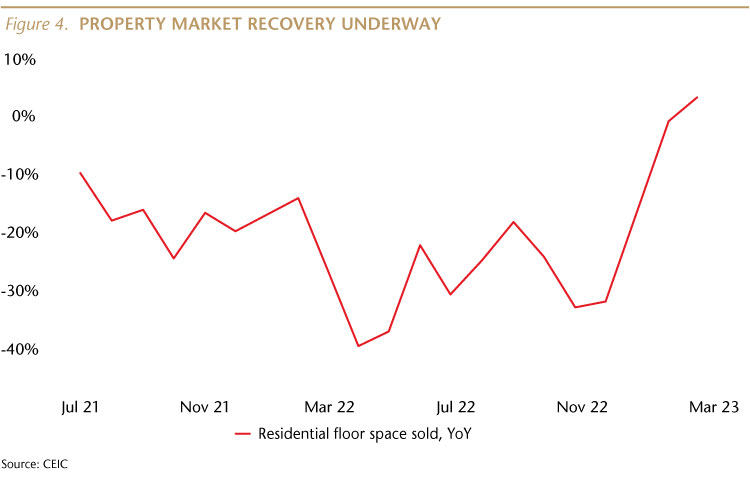

There was also a significant change in direction of the residential property market during the first quarter. With average mortgage rates down about 140 basis points (1.4%) compared to a year ago, and senior government officials encouraging owner-occupier buying, this improvement is likely to continue.

New home sales, which had fallen 27% YoY in 2022 on a square meter basis, were almost flat in January/February. In March, new home sales rose 3.5%, returning to positive YoY territory for the first time since July 2021. On a square meter basis, sales in March were equal to 94% of pre-COVID March 2019 sales.

Average new home prices rose 6% YoY in March, after increasing 4% YoY in January/February, following 12 consecutive months of YoY decline. Average prices are now 3% lower than two years ago, but 27% higher than five years ago and up 59% compared to a decade ago.

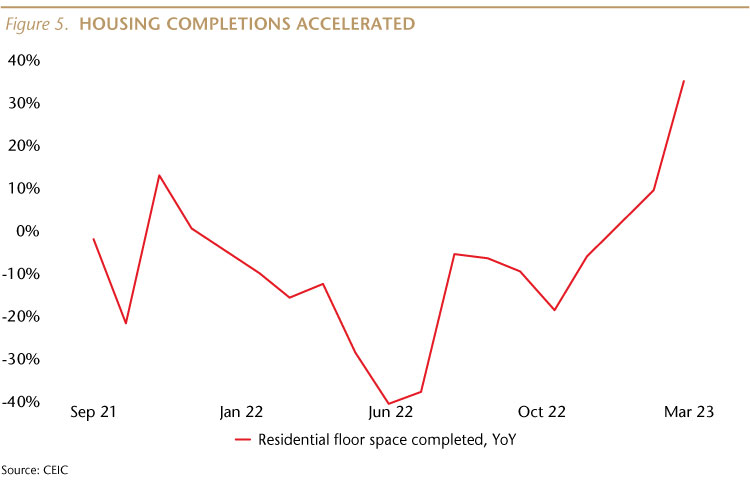

PROPERTY MARKET CHANGED DIRECTION IN 1Q23

New housing starts were down 27% YoY in March. However, new home completions continued to improve last month, up 35% YoY on a square meter basis, following an almost 10% rise during the first two months of the year, which reversed declines of about -6% in December and -18% in November 2022.

This activity is in line with credit data for March published by China’s central bank. Bank loans to households—including mid- and long-term loans, which are largely mortgages—rose strongly last month. Mid- and long-duration loans to corporates were also up, suggesting a recovery in CapEx spending.

Industrials

Industrial value-added also turned the corner in the first quarter, rising 3% YoY. This is a strong performance given the high base from a year ago, although it is still well below the 6.5% pace during the first quarter of 2019.

Improvements in steel and cement production suggest incrementally stronger construction activity.

Investment

Overall fixed asset investment rose 5.1% YoY in the first quarter, close to the 6.3% pace during the first quarter of 2019.

Trade

Exports only increased 0.5% YoY in the first three months of the year, as global demand softened. I expect this trend to continue, and the structure of Chinese economic growth to return to its pre-pandemic form. During the five years through 2019, final consumption contributed an average of about 63% of GDP growth, while investment accounted for more than one-third, and net exports contributed only about 1% of average annual GDP growth.

Government policies a potential risk

One of the key risks to the sustainability of the economic recovery now underway is that the government might adopt policies which stymie growth. That was a problem in recent years, but I think this is a very low probability risk now, because Xi’s clear focus is on supporting a consumer-led economic recovery, and because he is still cleaning up the consequences of past regulatory mistakes.

Xi said in December that he would “give priority to the recovery and expansion of consumption.” At last month’s National People’s Congress, the overwhelming focus of presentations by his team was on restoring economic growth to pre-COVID levels.

With the unemployment rate high (5.3% overall, including 19.6% for youth aged 16 to 24), Xi is highly motivated to keep his regulators from getting in the way of the entrepreneurs who are critical to achieving his target of about 5% GDP growth.

Some observers may be disappointed in this ‘low’ target, but keep in mind that 5% real growth would generate an incremental expansion in China’s nominal GDP which would be 25% greater than the expansion in pre-COVID 2019, when the real growth rate was 6%. The potential net expansion for this year in China would be roughly equal to the entire GDP of Mexico in 2021. Two other important points: First, this target was likely set at the Xi-chaired Central Economic Work Conference in December, when most of us didn’t expect the economic recovery now underway to begin until the second quarter. Second, strong growth in the first quarter and a lower base for the rest of the year means that China is very likely to surpass the 5% GDP growth target in my view.

Xi has directly addressed his policy mistakes of the past couple of years, and explained how he will correct them. This self-awareness and remedial action lead me to believe that new economic policy mistakes are unlikely in the near future.

Support for entrepreneurs

Xi has voiced support for the private companies that account for almost 90% of urban employment and most of the country’s new jobs, innovation and wealth creation. “It is necessary to expand the market access of private investment . . . and encourage and support the growth of the private economy and private enterprises,” Xi said in December. He directed officials to “solve problems for private firms.”

Xi’s new deputy, Premier Li Qiang, reiterated this point in a March press conference. While noting that some government policies last year made entrepreneurs “feel concerned,” Li said that now “private companies will enjoy a better environment,” with a “level playing field” that “treats companies under all types of ownership as equals.” He pledged support for entrepreneurs from “government officials at all levels.”

Support for big tech

Xi has also promised to reduce regulatory interference in the tech sector, saying that “it is necessary to vigorously develop the digital economy . . .and support platform companies [major tech firms] in leading development, creating jobs.” Other officials also voiced support for the tech sector, noting that industries such as IT, biotech and new energy vehicles now account for over 17% of China’s GDP.

Last month’s announcement that Alibaba (BABA) will split into six companies and explore initial public offering opportunities has broad significance for China’s markets. Given Alibaba’s past problems with the government, I believe that this was a carefully coordinated announcement—along with Jack Ma’s return to China the day before—with senior Party leaders. Premier Li Qiang, who has known Ma for many years, probably led the effort for Xi.

Coming shortly after the legislative session that was the formal kick-off of Xi’s new government, this is in line with my view that Xi is focused on supporting consumer-led growth and on restoring confidence of entrepreneurs, specifically the tech sector. This should also quiet speculation that Xi loves hardware companies and hates platform companies, which are the main consumer of hardware.

Support for property

Senior officials presenting at the legislative session also offered new support for owner-occupier homebuyers. The head of the planning agency said the government will “support people in buying their first homes or improving their housing situation,” and, as noted earlier, average mortgage rates are down about 140 basis points (1.4%) compared to a year ago. The government has also made available about US$79 billion in loans to help struggling developers complete construction of apartments which have already been sold.

Xi needs growth

It would be easy to dismiss much of this as just government talk. And, Xi must now deliver on all of this. But, these National People’s Congress presentations are usually good guides for what Xi wants to accomplish. Moreover, with a clear focus on reinvigorating the economy, Xi really does need to support consumers, entrepreneurs, tech companies, and new home sales if he wants to put growth back on its pre-COVID path.

And China is likely to remain the only major economy easing its monetary policy. Last year, “average interest rates on new enterprise loans fell to the lowest level on record,” according to one official.

U.S. – China relations: strained, but crisis unlikely

The second key risk to the sustainability of the economic recovery now underway is a potential crisis in U.S. – China relations, which would dampen further American and European investor sentiment towards Chinese equities. While I expect the political relationship to remain strained, I think a crisis is only a medium-level risk, because I expect Xi and Joe Biden to be pragmatic, and recognize that a further deterioration in relations would be detrimental to each of their economies, as well as to their political prospects. Additionally, an active approach towards investing in China, focused on companies selling goods and services to Chinese consumers, can help mitigate the impact of political strains.

Xi’s pragmatism

China has become rich and the Communist Party—including under Xi Jinping—has stayed in power because of pragmatic economic and social policies. Over the last three decades, the Party—including under Xi—has often made poor policy choices, but has usually changed course to a more pragmatic path. Recently, Xi has returned to a more pragmatic approach to the property market, to regulatory policy, to Chinese entrepreneurs, and to Washington.

These decisions by Xi signal that he understands that pragmatism is the best course for his country’s future, and for his own legacy. As a result, I believe U.S. – China relations will remain tense, but conflict, including over Taiwan, will be avoided.

When Xi and Biden met in Bali in November, both made serious efforts to put a floor under the rapidly sinking bilateral relationship. Both have since sometimes spoken critically about the other side, but Xi has not signaled an intention to cross critical U.S. red lines.

China has not, for example, violated U.S. and EU sanctions on Russia, and has not sold weapons to Putin. In my view, Xi is very unlikely to cross that red line in the future, as that would destroy China’s relations with Europe, as well as with the U.S. Xi understands the economic impact this would have, not only with respect to access to foreign technology, but because almost half of China’s exports go to Europe, the U.S., Japan and South Korea. Last year, Russia accounted for only 3% of China’s total imports and exports.

It is also very positive that the long-running dispute over audits of accounting workbooks for Chinese companies listed in the U.S. was resolved in December. The chair of the U.S. Public Company Accounting Oversight Board (PCAOB) announced that American “investors are now more protected because the PCAOB has been able to inspect and investigate audit firms in mainland China and Hong Kong completely.”

This agreement goes beyond keeping 200 Chinese companies trading in the U.S. It signals a desire, in my view, on the part of Xi, to avoid economic decoupling with the U.S., and to steady his relationship with Biden.

The balloon incident, of course, disrupted the more pragmatic approach taken by Xi, but this is not likely to permanently steer the relationship off course. The two sides have resolved far more difficult problems in the past.

In May 1999, the U.S. air force accidentally bombed the People’s Republic of China (PRC) embassy in Belgrade, killing three Chinese journalists and sparking large, anti-U.S. protests in Beijing. Rocks, ink bottles and Molotov cocktails were hurled at the American embassy, where I was working, and protestors set fire to the U.S. Consul General’s residence in Chengdu. But the two sides resolved the issue and six months later signed an agreement for China’s entry into the World Trade Organization.

In April 2001, a PRC fighter jet accidentally collided with a U.S. spy plane, resulting in the death of the Chinese pilot and an emergency landing in China by the Americans. The PRC held the 24 U.S. airmen hostage for 11 days, but then the issue was resolved, and the crew returned home. U.S. – China relations recovered relatively quickly.

Last month, Premier Li Qiang, acknowledged that “China and the U.S. are closely intertwined economically. We have both benefited from the other’s development.” Li said Beijing wants to “translate the important consensus” reached between Xi and Biden during their Bali meeting “into actual policies and concrete actions.” “China and the U.S. can and must cooperate.”

Xi pragmatic on Taiwan

I’m not very worried about China invading Taiwan, with my perspective informed by my time as the Taiwan desk officer at the State Department in the mid-90s, the last time China fired missiles near Taiwan.

The military risks for Xi Jinping attacking Taiwan would be huge, including the high probability of the U.S. joining the fight. Crossing 100 miles of sea would be far more difficult than Putin’s invasion of Ukraine. And the economic impact would be disastrous. China is dependent on imported oil, iron ore and soybeans (for animal feed). China also imports over 80% of the semiconductors it consumes, with about one-third—including all of the most sophisticated chips—coming from Taiwan. These supply chains would be shut down by the U.S. (and not easily replaced) if there were signs that Beijing planned an attack, crippling China’s economy.

This is why Xi emphasizes peaceful unification with Taiwan, and why there are no signs that China is preparing to attack or has a timetable for the use of force.

After meeting with Xi in November, Biden said, “I do not think there’s any imminent attempt on the part of China to invade Taiwan.” In January, the U.S. Secretary of Defense made similar remarks.

In a report published in March, the U.S. Director of National Intelligence (DNI) said the view of the U.S. intelligence community is that “Beijing will continue to apply pressure and possibly offer inducements for Taiwan to move toward unification and will react to what it views as increased U.S. – Taiwan engagement.” The report did not suggest that Xi was preparing to use force, and I continue to believe that this is very unlikely, in part because the downside risks—from both military and economic perspectives—outweigh any potential benefits to Xi.

Biden’s pragmatism

The American political environment will likely prevent a significant improvement in relations with China in the near future, but I believe that Biden understands that a sharp deterioration in the relationship would be harmful to U.S. economic and strategic interests. Stabilizing his relationship with Xi is a pragmatic choice for Biden.

Stable relations with China are important to the American economy. China is the U.S.’ third largest export market, and the top market for U.S. agricultural exports. Over 1 million American jobs are supported by exports to China.

China is the largest source of U.S. imports, and those products help keep inflation from rising faster, which is especially important to lower-income households, who spend a larger share of their income on tradable goods. About one-third of U.S. imports of electronics products come from China, where almost all of the world’s iPhones are assembled.

“China is central to global supply chains in a range of technology sectors, including semiconductors, critical minerals, batteries, solar panels, and pharmaceuticals,” according to the U.S. Director of National Intelligence (DNI). “China produces 40% of the world’s active pharmaceutical ingredients (APIs), the key ingredients in medicinal drugs.”

Biden’s “Cancer Moonshot” program, designed to reduce the death rate from cancer by at least 50% over the next 25 years, would benefit from continued cooperation with China. The two countries account for almost 40% of the world’s 10 million annual cancer deaths. U.S. – China (and other international) collaboration on clinical trials have proven to reduce the time it takes for new drugs to go from labs to American cancer patients by as much as seven to 10 years, according to Dr. Bob Li, an oncologist at the Memorial Sloan Kettering Cancer Center in New York, and a Senior Fellow on Global Public Health for the Asia Society’s Cure4Cancer project.

Progress on climate change also requires cooperation between Washington and Beijing. China is the world’s largest polluter, accounting for about one-third of global emissions, and is also a key part of the solution. “China’s global share across all of the manufacturing stages of solar panels now exceeds 80% and is set to rise to more than 95% during the coming years,” according to the DNI. China accounts for about 60% of global electric vehicle sales, 80% of fast charger installations, and over the last decade was responsible for about half of the increase in renewable energy production (compared to an 8% share each from the U.S. and Europe).

From a strategic perspective, Biden is aware that last year, 17 of the 29 American NATO partners conducted more trade with China than with the U.S. In Asia, key American military allies Japan, South Korea, Australia and New Zealand all trade more with China than with the U.S.

The March DNI report also put Xi’s strategic objectives into perspective, concluding that while he has a vision “of making China the preeminent power in East Asia,” his global vision is limited to being “a major power on the world stage,” not replacing the U.S. as the world’s superpower.

It’s also worth noting that Xi faces significant strategic constraints outside of his backyard. China has a mutual defense treaty with only one country (North Korea) and has only one overseas military base (in Djibouti). The U.S. has seven defense treaties (including with Australia, New Zealand, Japan, South Korea and the Philippines), encompassing 51 countries. As of 2021, the U.S. controlled about 750 overseas military bases, located in about 80 foreign countries, including many in Asia.

Back in 2019, during the final stage of the U.S. presidential campaign, two of Biden’s foreign policy advisors, Jake Sullivan and Kurt Campbell, wrote an article in Foreign Affairs which explained the rationale for a pragmatic approach to Beijing. Sullivan, now Biden’s National Security Advisor, and Campbell, now Deputy Assistant to the President and Coordinator for the Indo-Pacific, wrote, “Despite the many divides between the two countries, each will need to be prepared to live with the other as a major power,” and that “it would be misguided to build a neo-containment policy on the premise that the current Chinese state will eventually collapse, or with that as an objective.”

“China is deeply integrated into the world and intertwined with the U.S. economy,” the two Biden advisors explained. “As a global economic actor, China is central to the prosperity of American allies and partners.”

I expect that Biden agrees with their conclusion: “Global problems that are difficult enough to solve even when the United States and China work together will be impossible to solve if they fail to do so. . . The goal should be to establish favorable terms of coexistence with Beijing.”

In an April 20 speech, Treasury Secretary Janet Yellen suggested that the Biden administration is now taking a more constructive approach to Beijing. “We seek a healthy economic relationship with China: one that fosters growth and innovation in both countries.” She said that national security actions taken by the U.S. “are not designed for us to gain a competitive economic advantage, or stifle China’s economic and technological modernization. . . The United States does not seek competition that is winner-take-all. Instead, we believe that healthy economic competition with a fair set of rules can benefit both countries over time.”

Yellen also stated that, “Our innovative culture is enriched by new immigrants, including those from China – enabling us to continue to generate world-class, cutting-edge products and industries.”

Andy Rothman

Investment Strategist

Matthews Asia