Q1 2024 CIO Review and Outlook

CIO Sean Taylor says macro uncertainty may moderate in the coming months, placing greater importance on active investing for generating alpha in emerging markets.

Subscribe NowKey Takeaways

- Natural recovery is taking hold after COVID. Economic growth is picking up and being driven by domestic consumption.

- Emerging markets are a cyclical asset class. When the U.S. starts cutting rates, many emerging markets’ central banks will in turn be able to cut, in our view, which should prompt a cyclical pickup.

- We expect the second half of the year to yield slightly better news for China. We think earnings will continue to improve and there will be more initiatives to support the consumer.

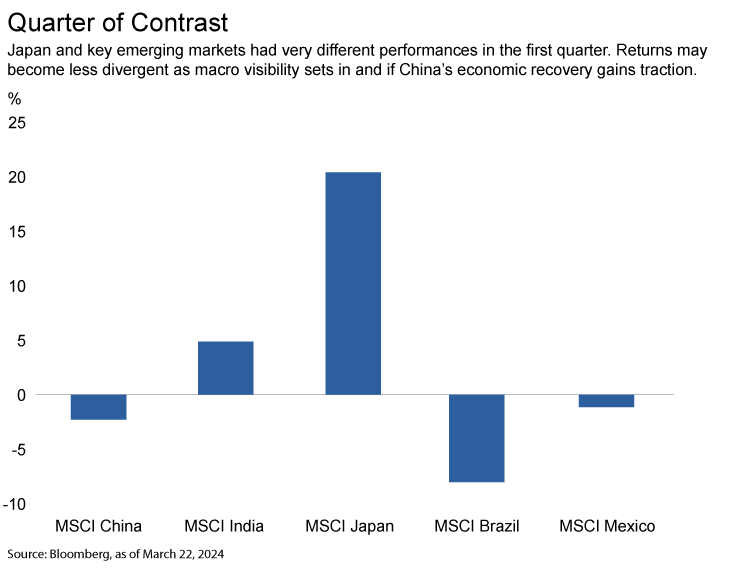

At the beginning of the year, we took the view that emerging markets in Asia as well as Japanese equities would perform well but that the first few months would be unsettled. That's largely how it has played out.

China had a very poor start as its economy continued to struggle amid weak consumer sentiment and severe challenges in its property sector. Elsewhere, market performances were contrasting. India, the strongest structural story in emerging markets, in our view, performed well in the quarter but it was overshadowed by a barnstorming Japan. The markets of Latin America, on the other hand, were more volatile, Brazil in particular.

The main reason for our expectations of volatility was related to the global macro environment, specifically expectations for U.S. interest rates. In December, the markets were pricing in 160 basis points (1.60%) of cuts by the Federal Reserve. Those expectations have now reduced to 75 basis points (0.75%). It’s a significant shift and more cyclical markets, like those of Latin America which are exposed to global supply chains, were adversely affected in the quarter. As we look to the remainder of the year, we think this new clarity in the macro environment will cause volatility to dampen and that should be very positive for emerging markets.

Promise in Asia

Looking at the regions in more detail, starting with Asia, India’s equity market as a whole did well but valuations are elevated in many areas and we saw a pullback at the latter end of the quarter, particularly in small caps. As a consequence, for now, we are leaning a little more to the large caps where the market is more predictable. Long term, we are very positive on India’s economic growth and positive that the mechanisms are in place for more infrastructure and more property investment and for a broadening out of the economy. Consumption is taking time to pick up after the pandemic but it is supporting economic expansion and better earnings growth especially in mid-cap areas. While we expect some consolidation in India equities, for active investors like ourselves, we think it may be an opportunity to add exposure.

When global interest rates start to come down, South Korea is another market we anticipate adding more exposure to, particularly on the cyclical side. We are also seeing a growing pressure from regulators, the government and investors generally for South Korean companies to improve capital efficiency and governance and, in doing so, release more value to shareholders. Another tailwind is that South Korea is uncorrelated to the economic path and challenges of China, in our view.

“We are very positive on India’s economic growth and positive that the mechanisms are in place for more infrastructure and more property investment and for a broadening out of the economy.”

Japan’s re-rating

Japan really has become a poster child for where improvements in capital efficiency can take you. After the government’s edict last year forcing Japanese corporates to start using their balances sheets more efficiently to improve corporate value, we’ve seen some momentous increases in buybacks, dividends and payout ratios. To date, Japanese equities have turned in an incredible performance and it’s largely because local investors are returning to the market encouraged, in our view, by the capital reforms Japanese companies are making. This investor inflow has already driven a re-rating of price-to-earnings multiples.

At the macro level, these are also significant times for Japan. The Bank of Japan’s recent decision to end its negative interest rate policy is a key signal to investors that for the first time in a long time the central bank sees a growth momentum taking hold and that it is prepared to be relatively dovish. As we look ahead, we may see Japanese equities consolidating but over the longer term we believe Japan is a very good opportunity.

Indices are unmanaged and shown for comparative purposes only. It is not possible to invest directly in an index.

A market that has supported many of our portfolios in the first quarter is Taiwan, largely because of its strong ties to the rapidly growing contribution of generative artificial intelligence (AI) to economies and global trade. Multiple semiconductor makers and computer server manufacturers are located in Taiwan and many are embedded in AI-related supply chains. Their main market is supplying the hardware needs of the large U.S. tech companies and we see this demand as sustainable and expanding.

On a more general point, whenever there is a global innovation shift in Asia, the region has demonstrated a tendency to leapfrog to achieve growth. Similarly, we see a long runway for the take-up of AI from a business, industry and consumer standpoint. In manufacturing, for example, we think AI could be a trigger for real competitiveness in certain markets like China and Malaysia. And it is impacting other sectors, like financial services, where a market such as India is already a significant beneficiary.

Leveraging LatAm

Some key markets in Latin America were challenged in the quarter. Brazil and Mexico were ahead of the curve in raising interest rates to combat inflation but their economies are now contending with prolonged and elevated interest rates which will likely be cut in lockstep with the measured strategy of the Fed. Another headwind for Brazilian equities has been softness in some commodity prices, particular lithium and other materials related to the electric vehicle (EV) battery market due to a slowdown in demand from China. There has also been a degree of uncertainty over the interventionism of the Lula government. That all said, the Brazilian economy is very entrepreneurial and innovative. Financial services and fintech companies, for example, are solid long-term themes, in our view. We would also say that Brazil has the potential to be a structural growth story like India, in part driven by the government’s infrastructure, energy and transportation programs.

Mexico’s market fared better than Brazil last quarter. Post COVID, the economy has seen gathering momentum from overseas companies investing in the country, building units and plants to gain proximity to end markets in the U.S. or to sell directly into Mexico. Like Brazil, Mexico is full of innovative companies, and we are seeing disrupters emerging in sectors, including real estate and retailing. Like Brazil, however, Mexico is also a cyclical economy and our portfolio positionings are cognizant to the expected cadence and timing of rate cuts, as well as to the political environment, including the upcoming election in June.

“Last year, Chinese government policy over promised and under achieved. This year, we think the government wants to under promise and over achieve.”

China’s prospects

As for China, at the start of the year we saw steep falls in some of the smaller indexes. Economic recovery has been much weaker than the market expected and there are only incremental signs that China’s property market is beginning to turn a corner. But we have started to see some positives. Some of the government’s efforts have started to gain traction, such as its initiatives to support the stock market by buying equities and restricting certain sales and short selling. And, in fairness, the government has also been injecting a fair amount of fiscal spend into the economy, especially at the local government level.

The question is whether the recovery in equity markets that we saw in the quarter is sustainable. We would say there is an active investment risk in being too underweight in China but we're not yet seeing a fundamental catalyst to be very overweight. Earnings need to pick up and there needs to be more support for the consumer. So we are still in a cautious frame of mind, tinged with some optimism. While last year Chinese government policy over promised and under achieved, this year we think the government is seeking to under promise and over achieve. Of course, the one potentially destabilizing variable on our radar is geopolitics, particularly with the U.S. election approaching.

“Generating alpha in 2024 and is going to be down to stock picking and country selection. It’s a very, good environment for active investors.”

The need to be selective

Putting it all together, as we look ahead to the rest of the year we see three reasons to be positive on emerging markets. The first is the natural recovery that is taking hold after COVID. Economic growth is picking up and that’s really being driven by domestic consumption. Secondly, emerging markets are a cyclical asset class, in our view, and so when interest rates are cut in the U.S., many emerging markets’ central banks will in turn be able to cut and so we should get a cyclical pickup aided by an expected weakening of the U.S. dollar. If signs increase that rates will begin to be cut in June, then this pickup will start to be factored in the markets, which will be a positive. Thirdly, we expect the second half of the year to yield slightly better news for China. We think earnings will continue to improve and there will be more initiatives to support the consumer. So we think China should become a structurally better story.

And China’s plight in many ways highlights what I believe to be the key phrase for the rest of the year: the need to be selective. The big macro picture is pretty set. The U.S. economy is doing better than people thought and rates will start to come down at some point as inflation starts to tick down. Inflation has been a little stickier-than-anticipated but prices are going in the right general direction. Thus, generating alpha is really going to be down to stock picking and country selection. It’s a very good environment for active investors. Being able to pick the stocks that are growing, see where earnings are picking up, and identify companies that are working with shareholders—with stock buybacks and paying out more in dividends—will be key.

A number of markets have done well so far this year but we are now at the stage where it's not just necessary to buy exposure to those markets but it’s about buying the right exposure at the right price and with a visible growth trajectory. We are comfortable with that. It’s in our DNA.

Sean Taylor

Chief Investment Officer